23 sep Why decentralization matters – A legal perspective

By WatsonLaw and Flipside Governance. Special thanks to Balloonist for the detailed and invaluable feedback.

1. Introduction

DAOs are alive. They offer a fast, low cost, and efficient way to bootstrap communities and businesses with international contributors that can participate as much — or as little — as they want.

DAOs offer a radical departure from traditional company and organizational structures that haven’t changed much since the industrial revolution and reflect the needs of manufacturing organizations more than of modern, collaborative knowledge workers.

But DAOs operate in a strange kind of regulatory vacuum, until legislators come forward with clear intentions and actual policy. The concept of a decentralized and autonomous organization is so new, that regulatory processes have not caught up.

DAO governance and contributors are facing existential challenges in setting up structures that can last. Regulatory guidance has been vague at best, most likely because government bodies don’t want to pigeonhole themselves. At the same time DAOs have not communicated their intentions and their desires for legislation in a cohesive and structured way. DAOs have not, for example, formed substantial lobbying or educational cohorts that could influence legal opinions yet. We fully expect that to happen in the near future as there’s simply too much at stake to just take it as it comes.

Despite the absence of clarity, we have studied numerous legal position papers from VCs, independent organizations and government bodies world-wide and discovered one overarching trend: Decentralization.

Decentralization

Every paper or publication that we read recommended exemptions to legislation for fully decentralized organizations. And we could discern some patterns about what constitutes decentralization that DAO developers or governance should be aware of.

Our report will lay out the criteria for decentralization we have gathered. We want to empower governance and token holders as well as DAO developers by mapping a spectrum of decentralization, with a pure DAO on one end and owner-controlled organizations on the other.

For the purpose of this report, we will use the term ‘organization’ to describe the entities or protocols which may or may not qualify as DAO’s.

We’ll also get into specific activities and how they can be designed to make a DAO safer from regulatory risk. Nothing in this report should be construed as legal advice, however. It also doesn’t necessarily reflect the legal position of Flipside Crypto, Inc. We are simply summarizing the research we have made and hope that it is informative for our readers.

We are aware that DAOs have many different forms and functions, and not every DAO can and will be able to operate in a completely decentralized fashion. Our spectrum can nevertheless serve as valuable input in navigating regulatory compliance.

For the purpose of this research, we will look at DeFi DAOs, or other DAOs that interact with users’ assets. DAOs that are formed to organize kid’s dance rehearsals, or DAOs that are formed to coordinate social gatherings are very different animals. We’ve chosen to focus on DeFi because these organizations are the most prominent examples and also concern the most value.

2. Why decentralization matters

DAOs offer distinct advantages that matter on a civilisational level. They are egalitarian in their nature. Contributors are often anonymous or use pseudonyms and avatars, which breaks traditional power dynamics and allows equal access to opportunities regardless of country of origin, sex, creed, or faith.

Should a DAO incorporate, say, in a jurisdiction with strong employee rights, it would likely have to doxx, or de-anonymise, its contributors in order to employ them or formulate contracts. This would render some of the advantages of anon-culture void and null. A DAO might still choose to travel that particular route, in order to protect its members from legal fines. Other concerns would be doing due diligence on contributor backgrounds to avoid situations where past legal issues come back to haunt a DAO at the most inopportune time, like what 0xSifu’s past did to Wonderland and Time.

DAOs are very easy to start and allow rapid experimentation plus access to a global talent pool.

As the pace of changes accelerates and the magnitude of challenges rises, DAOs offer a way for society to adapt at lightning speed.

On the other hand, regulators have an interest in collecting taxes due and protecting consumers from large-scale fraud, as well as ongoing concerns about money laundering and circumvention of sanctions. DeFi DAOs, especially, have to make sure to address these concerns. At the same time regulators should take one step back and observe, so they can regulate in a fashion that maximizes the vast potential that autonomous organizations represent.

Decentralized operations offer a clear way to achieve both, staying outside of regulatory demands while remaining flexible and nimble enough to charge forward with necessary experiments and initiatives. Decentralized operations are synonymous with self-custody of assets. If the DAO has control over users’ assets at any time it assumes responsibility, and this is what regulators are concerned about.

Across all the papers we have studied, the chorus was always that as long as an organization is decentralized enough, it does not fall under the purview of a single jurisdiction and hence does not need to be regulated. In some ways it can be argued that a pure, autonomous, immutable DAO only consisting of smart contracts cannot be regulated, since there is no responsible entity that can be fined, or even cited to a court hearing.

Just exactly how much decentralization is enough varies from activity to activity as well as from legislation to legislation and from paper to paper. Maybe a thought experiment can help to illustrate the terrain on which we operate.

Imagine a DAO with immutable and non-upgradeable smart contracts that perform certain functions. Take something like RAI, a crypto-collateralized stablecoin, as an example. Let’s say the parameters of our — fictional — DAO can only be adjusted by a diverse and distributed quorum of users and the whole process is immune to human intervention. Collateral in — Stablecoin out. Stablecoin in — Collateral out. Nothing more, nothing less. All governed on-chain by its users without control by developers or whales.

Our theoretical protocol would be a pure, autonomous DAO. It is what is often referred to as a pass-through entity which does not accrue profits itself, and where no single person or group controls the whole. The smart contracts continue to run even when all the developers and every user that interacted with the DAO has been sentenced to jail. There is no entity that can be regulated, and as such the DAO exists outside of regulation.

Then imagine a newfangled NFT speculator DAO where a tiny and exclusive group of ten members pools funds to buy NFTs and later sells them for a profit. Earnings go into various DeFi strategies that are maintained by a yet smaller subgroup and further amplify profits.

The DAO consists of a group chat and a multi-signature wallet, like a Gnosis Safe.

This is basically a for-profit entity without legal formation. And it’s probably apparent why regulators want to have their share of the pie in the second case. Of course, users making a profit still have to pay taxes in the first case, but not the DAO as an entity, which is what matters to DAO governance.

These two extremes define the far ends of the spectrum of decentralization. We have illustrated the extremes so far, but what is between them?

3. Degrees and aspects of decentralization

The question whether an organization is truly decentralized is of the utmost importance for a legislator. To regulate a decentralized organization, there has to be a legal subject, someone that controls at least parts of the DAO that can be targeted by execution. The lack of these subjects poses challenges for policymakers. The European Central Bank (“ECB”) proposes to tackle the ‘intersection’ between the decentralized organization and the centralized outside world.

Only truly decentralized organizations can then stay outside of the regulatory perimeter. To assess whether an organization is truly decentralized or whether these centralized ‘intersections’ are present, regulators have to take into account multiple aspects of organizations. In this chapter we set out to identify the main aspects within an organization in which decentralization can take shape, and the main ways in which decentralization takes place within these aspects. Some supervisors have already given guidance on the aspects that they consider to be important, and in literature there are already discussions about what makes an organization truly decentralized. Actual DAO founders are well advised to seek competent counsel. The future of DAO law will be forged in courts at least as much as in parliaments.

3.1 Supervisory guidance

We will cover some of the supervisory guidance released by regulatory bodies. First, we’ll look at the Financial Action Task Force (“FATF”). The FATF is the global money laundering and terrorist financing watchdog. The FATF sets international standards to prevent these illegal activities and the harm they cause to society. The FATF functions as a policy making intergovernmental body.

3.1.1 Financial Action Task Force — Anti Money Laundering

Neither the FATF nor any other supervisory body determines whether an organization is truly decentralized based on marketing terms or self-identification. As the Financial Action Task Force (“FATF”) sets out in her Updated guidance for a risk-based approach for Virtual Assets and Virtual Asset Service Providers situations occur in which, although the organization markets itself as being decentralized, the organization actually includes a person with control or sufficient influence.

The FATF maintains its own definition of organizations they call Virtual Asset Service Provider (“VASP”), which is a somewhat similar, yet less broad, term than the Crypto-Asset Service Provider (“CASP”) which has been set out in the new Markets in Crypto-Assets regulation (“MiCA”).

The FATF states that creators, owners, operators or other persons who maintain control or sufficient influence in the organization, may fall under the definition of a VASP, even if the organization seems decentralized. To determine whether this is the case, the FATF sets out some illustrative characteristics:

- Is there control or sufficient influence over assets or over aspects of the service’s protocol by any party?

- Is there an ongoing business relationship between the users and any party?

- Does any party profit from the service?

- Does any party have the ability to set or change parameters to identify the owner/operator in a decentralized arrangement?

These criteria set out by the FATF can be utilized to identify a centralized party within the arrangements of the organization. Even if the organization itself seems decentralized, the input or output of the organization can be organized through a central party. As the FATF sets out, for example, even if a decision is made in a decentralized manner, but the same centralized third party is always used for the implementation of the decision off-chain, not the entire process is decentralized.

Another example is when the parameters of the decentralized organization are set beforehand. Then, even though the organization moves in a decentralized manner, the parameters in which it moves are set by a centralized party. These centralized parties, either at the input side of the organization or at the output side, can be identified. This means that not the entire process is decentralized.

3.1.2 Financial Stability Board

The Financial Stability Board (“FSB”) is an international body. It monitors and makes recommendations regarding the global financial system. The FSB has published a report on decentralized finance (“DeFi”) technologies. The FSB identifies three broad forms of decentralization within financial services:

- Decentralization of decision-making

The decentralization of decision-making is the move away from single intermediaries towards a system in which a broad set of users can make decisions whether to undertake transactions.

- Decentralization of risk-taking

The decentralization of risk-taking is the move away from retaining risk, like credit risk and liquidity risk, on the balance sheet of a single intermediary towards more direct matching of individuals.

- Decentralization of record-keeping

The decentralization of record-keeping is the move away from centrally held records towards records held and verified on a distributed ledger, creating an immutable audit trail.

The FSB states that organizations displaying all three forms of decentralization in full seem unlikely to achieve economically significant scale in the near term. This means full decentralization of decision-making, risk-taking and record-keeping. It has found that the majority of existing organizations retain some degrees of centralization in either one or two of the three areas.

3.1.3 International Organization of Securities Commissions

The International Organization of Securities Commissions (“IOSCO”) is a global standard setter for regulations of securities markets. IOSCO has also described decentralization in its public report on decentralized finance, stating that the matter is not as straightforward as organizations either being centralized or decentralized. IOSCO describes decentralization as a spectrum in which multiple aspects of a product or a service can reside.

These various aspects such as ownership, voting power, control of assets, network design and off-chain infrastructure can all exhibit decentralization to a different degree. To determine the level of decentralization, and thus the actual qualification as a DAO, one has to look at all different levels within every aspect of the organization.

It is important to determine which aspects do and do not involve central actors or parties. Moreover, it is also important to identify whether an individual’s decisions impact only their own choices and actions using the protocol or whether an individual has the ability to impact the protocol itself.

3.1.4 Bank for International Settlements

The Bank for International Settlements (“BIS”) is an organization that promotes global monetary and financial stability through international cooperation. BIS has written a report on what they call the ‘decentralization illusion’. In this report the BIS argues that some form of centralization is inevitable.

First, because organizations are unable to draw up (smart) contracts that cover all possible eventualities. In blockchain based organizations this takes the form of algorithm incompleteness, meaning that it is impossible to write code covering all possible eventualities.

Secondly, because following a vote on a certain subject within the organization, the outcome has to be implemented. This can be done via smart contracts, so-called admin keys. Although these are time-locked and require multiple signatures, they still represent a form of centralization. When these do not exist within the protocol, the protocol itself is immutable.

Lastly, BIS also argues that certain features of the blockchains that the organizations are built upon favor the concentration of decision power with large token holders. The validators, also known as ‘miners’, need to be sufficiently incentivized to not commit fraud. Within proof-of-stake blockchains, validators with more tokens have a larger chance of validating the next block and therefore receiving compensation, this ultimately leads to concentrations of validating power and thus concentrations of implementing power, centralizing the organization in the process.

3.2 Literature

DAOs differ in many ways from existing legal organizational structures. Membership can be acquired instantly, while in traditional structures people have to be formally appointed based on pre-defined roles. Assets can be moved instantly, while in traditional structures there is a need for interaction with third party intermediaries and institutions. (See this paper for more depth.)

There can be multiple ways to decentralize aspects of an organization. It can, for instance, be partially decentralized. A decentralized decision-making process can be introduced for a certain subset of decisions within a centralized organization. This could allow for stakeholders to influence a particular product, while other products remain under centralized control.

An organization can also consist of multiple, small ‘DAOs’, which form a DAO for a department within the organization, allowing to keep specialists within their own domain, but not limiting a person’s potential influence to that specific domain. A third means of decentralization is secondary decentralization. This is the case when a centralized organization gradually becomes more decentralized, ultimately shifting into a DAO. This can be done by slowly transferring ownership and governance rights to future holders. In the case of secondary decentralization, for a period of time there is still a central party that can adhere to regulations. The question however remains how decentralized it truly becomes, when a central board decides how and when to decentralize the organization.

In literature, many characteristics of DAOs have been identified. In an analysis of various descriptions of DAOs in literature, four main categories of characteristics were defined:

- Functional characteristics, which includes the characteristics that focus on the functional side of DAOs in themselves, being the most common functionalities.

- Governance characteristics, which includes the characteristics that describe the decision-making process and execution.

- Operational and legal characteristics, which includes the characteristics that describe an operational element or propose a legal form; and

- Technical characteristics, which includes the characteristics based on the technical setup of the DAO.

3.3 The Spectrum of Decentralization

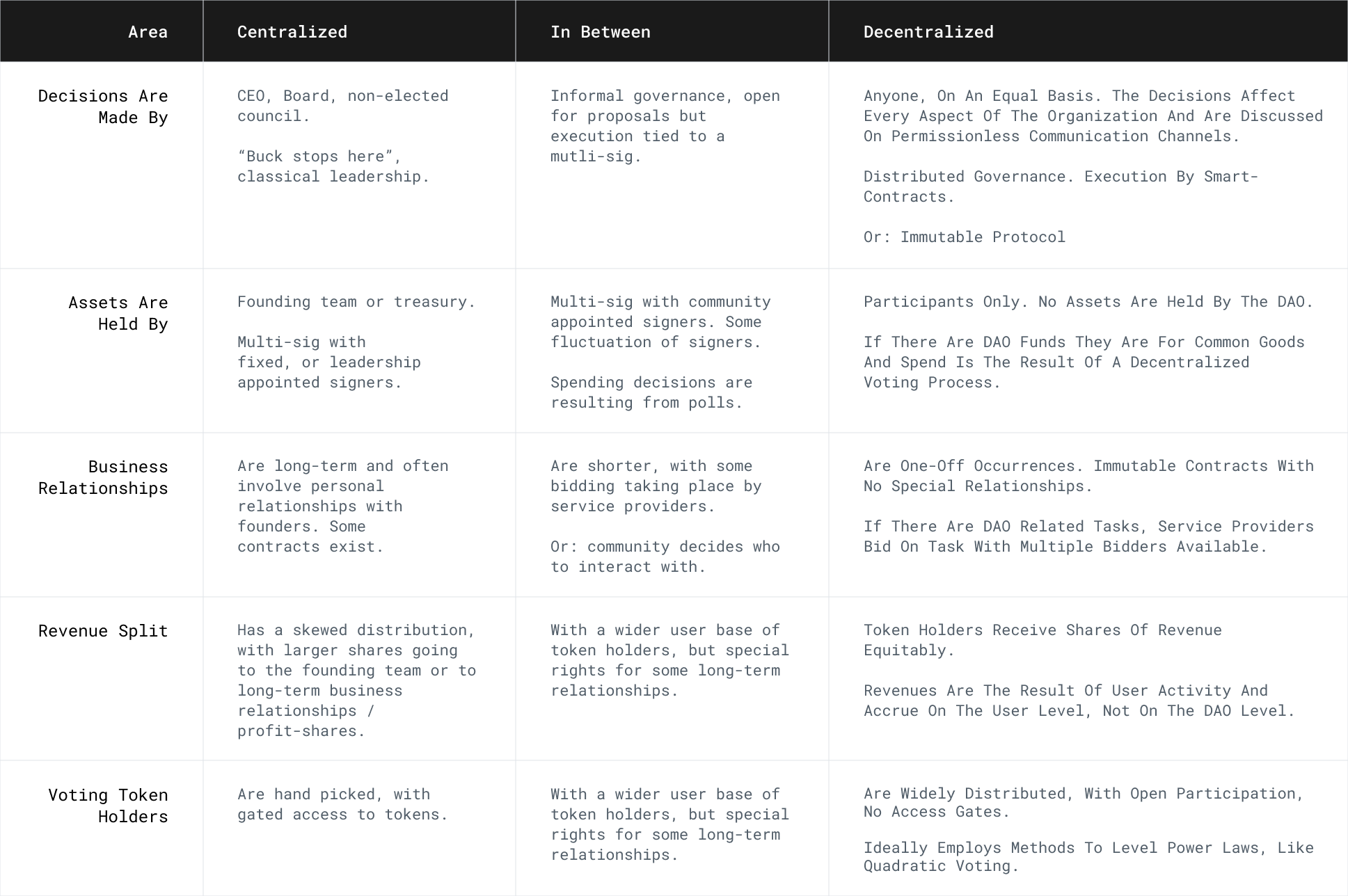

For the purposes of this article, we have identified the following main aspects within an organization on the basis of which the level of decentralization, and thus the organization actually being a DAO, can be determined:

- Decision-making

- Treasury management

- Business relationships

- Profit/Revenue split

- On-chain and off-chain infrastructure

- Division of tokens and participation

These aspects of an organization can be categorized from centralized to decentralized. In the following we will address how the degree of centralization in either of these aspects can be determined.

Decision-making

The decision-making process within a decentralized organization consists of two elements: proposing and voting. Both of these elements have to be decentralized in order for the decision-making process to be fully decentralized. The voting within a DAO is done by holders of the governance token. Multiple voting processes can be identified within a decentralized organization. The first is token-weighted voting. This is a process in which the degree of influence is based on the number of tokens a holder has. Another voting method is time-weighted voting. In this process, the amount of votes per token is based on how long that token has been in the current holder’s possession. A third method is the method of quadratic voting. This method gives large token holders greater influence per token within the voting process. A fourth method some DAO’s work with is based on one vote per person, which does not take into account how many tokens a person possesses.

The proposing process also plays an important role within the decision-making of a DAO. An organization cannot be truly decentralized without every token holder being able to make proposals for the organization. If the voting process is decentralized, but the proposals are made by a small group, this small group has all the influential power within the organization. Nothing is being voted on, without the approval of the group of persons with the ability to propose.

The role that the decision-making process plays within the protocol is also of influence in the assessment of the decentralization of an organization. The decision-making process has toaffect every aspect of the organization, for example the management of the organization and the overseeing of the entity and developers of the smart contracts and the protocol. It is possible within a decentralized organization that while the decentralized protocol may mitigate censorship and centralized control, it can still be dependent on the development of the protocol and the functionality of its creators and first investors.

For the decision-making process and the discussions leading to decision-making, the communication channels on which the organization relies are of importance. If an organization wishes to be truly decentralized, it cannot rely upon permissioned communication channels. For example, communication via social media tools. This may give rise to information asymmetry within the decision-making process of the organization. To be truly decentralized, the communication channels have to be available to anyone. If new front-ends can be made available by anyone to circumvent certain censorship that has been too intrusive, it makes the process more decentralized.

Treasury management

The control over the organization’s assets and funds has to be fully in the hands of participants in the DAO. Every participant has to be able to vote on all decisions regarding the assets and funds. When the custody over the assets and funds has been appointed to a more centralized party, the control of assets is not fully decentralized. The treasury has to be fully transparent and accessible to all participants.

Business relationships

One aspect that can have influence on the degree of decentralization within an organization is the existence of long-term business relationships with a single party, by which we mean long-term exclusive cooperation. If an organization is bound to the long-term usage of a certain party’s services, this can be the result of a premeditated act of centralization. Any person has to be able to propose entering into a business relationship with the DAO to the token holders, for them to vote on.

Profit/revenue split

To know whether the profit from a DAO is decentralized, multiple aspects have to be looked at. A decentralized organization can profit from its activities, but third parties can also profit from the existence of the DAO.

First and foremost, it is important to look at the profit split between governance token holders. If profit is made from a DAO, it can only be truly decentralized if the profits are split equally among all token holders. If there is a division between profit rights contained within a token, or if a certain group of participants gets a percentage before the profit is split, the profit division is not truly decentralized.

Another way of profiting from a DAO is related to the existence of long-term business relationships as mentioned above. If decisions are made decentralized, but the same third party or limited number of third parties act out the decisions made by the DAO off-chain, then the same parties always profit from the existence of the DAO. For a DAO to be completely decentralized within the profit aspect of the organization, the people who profit from its existence and the work that comes from the DAO have to be decentralized as well. This means that everybody is able to profit from the DAO’s existence.

On-chain and off-chain infrastructure (governance)

The governance of an organization is the combination of all rules, procedures and processes that maintains the organization. DAO governance consists of two factors, ‘on-chain’ governance and ‘off-chain’ governance. For the on-chain governance, decisions are made by all tokenholders, with the protocol automatically incorporating the results. An important part of the on-chain governance is the protocol on which the organization is built. Blockchains can be divided into two subcategories: permissioned and permissionless blockchains. In a permissioned blockchain, software is deployed by pre-defined actors and a series of predefined accounts. A permissioned blockchain can therefore be regarded as centrally controlled and coordinated. Permissionless blockchains allow multiple participants to coordinate decentralized, with permissionless participation. In a permissionless blockchain, the protocol is free to anyone to enter and everybody is able to submit and validate transactions. (See this paper) Truly decentralized organizations can therefore only be built on a permissionless blockchain.

The off-chain governance is more complex. This governance does not only include the token holders, but also developers and a wider community of persons wishing to interact with the organization. Even if the on-chain governance is completely decentralized and a vote leads to an agreement, the agreement still has to be acted upon. The reaching of the agreement has to be validated, and validation can be done by a small decentralized group because of the inevitable compensation structure of proof-of-stake blockchains. And even if these validators were decentralized, and the vote was decentralized, if it concerns an off-chain activity, the agreement still has to be acted upon by a person outside of the blockchain.

Division of tokens and participation

The final aspect of an organization that can indicate the level of decentralization within the organization is the division of tokens and the participation of the organization. Decentralized organizations base their decentralization on a person’s ability to become a participant and to buy governance tokens. However, the existence of the possibility for a person to become a participant in the organization and the ability for a person to buy governance tokens does not necessarily mean that an organization is decentralized.

First of all, for an organization to be truly decentralized, no limitations can be put upon the ability to become a participant. Anyone wanting to join must be able to join, in order to prevent the organization from being a select group that can be defined as some form of a partnership. There also has to be a minimum number of participants. When a decentralized organization consists of just a small number of participants, a small group can issue changes with a majority vote. Although no minimum amount is set in stone, some literature suggests a DAO should consist of at least 20 participants.

Another important aspect is the division of the governance tokens. Even if anyone can become a participant, and the group of participants consists of a large number of people, the tokens can be distributed in a way that a small group, or even one person, can issue changes. An organization can become more decentralized with a good governance token distribution.

It is also important that participants may ‘self-custody’ their tokens. This means that they can determine what they do with their tokens without anyone being able to interfere. They can, for example, transfer the tokens away from the protocol without anyone having any right to it.

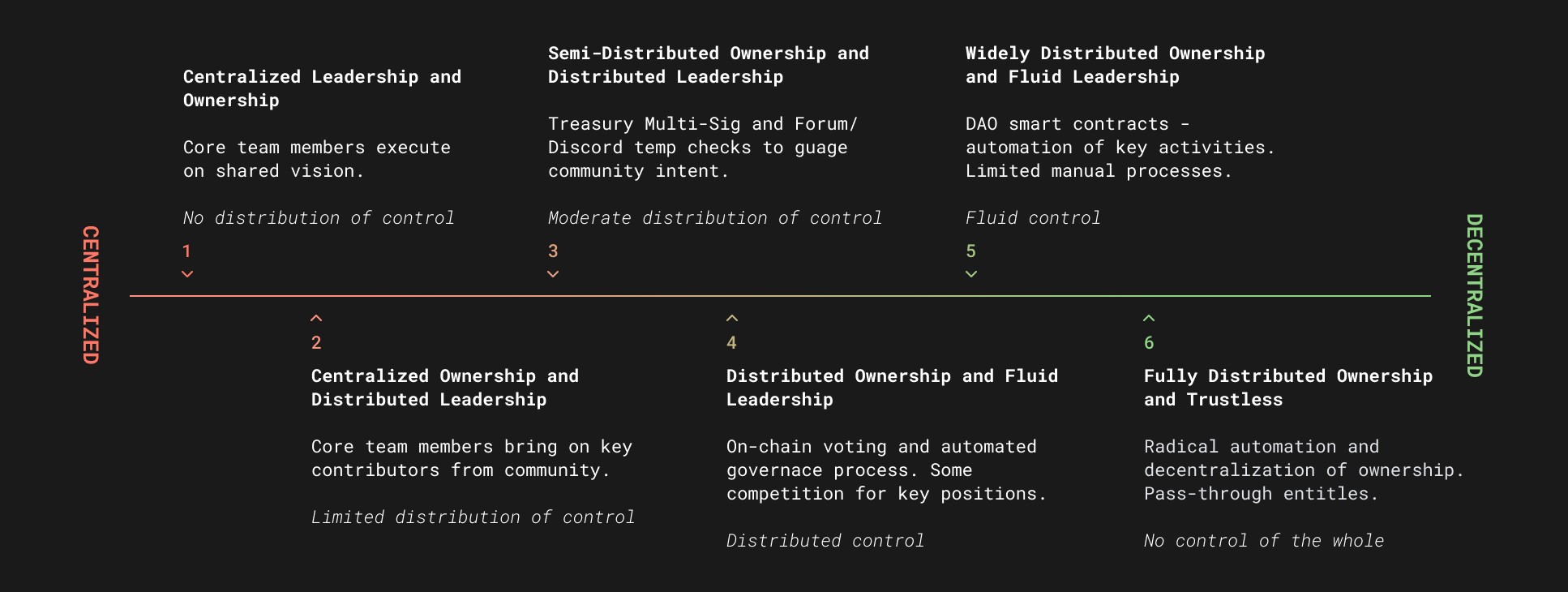

4. Decentralization at a glance

Now that we have a clearer picture of what decentralization means in legal terms, we wanted to distill our findings into an easily understandable graphic. We have shown that decentralization is not one thing, but a process and exists on a spectrum.

The main aspect for legal definitions of decentralization is control, because control ultimately governs responsibility and whether or not regulatory bodies even have the possibility to enforce legislation with some cost effectiveness. Another important aspect is counterparty risk, which can be viewed as tightly coupled to control. If users interact with protocols that are still controlled by others, there is counterparty risk to people. In the case of immutable smart contracts there is only counterparty risk to code. The latter is very different from the former, in that code behaves deterministically and can be read and understood to construct a complete risk profile, at least in theory. The same cannot be said for human counterparties.

Starting at (1), we see a fully centralized entity with some form of audience participation. The audience might have a say in the product roadmap or even get to decide which features ship first, but ultimately all the control is in the hands of the company’s leadership. If the company is calling itself a DAO or is operating without a formed entity, it is still a DAO in name only.

Moving towards decentralization, at (2), the company starts to push important decisions to the edges and empowers community members with more critical roles. If a group of people have to get together to sign a multi-signature wallet to effect spending, for instance, or to approve contract changes, then control is bundled, even if these actors have no other ties apart from these duties. It could be argued that (3) is really a kind of general partnership with novel ways of coming together. Case-law will determine how these kinds of DAOs will fare under various jurisdictions.

If competition for key contributor roles doesn’t result in frequent changes to key positions, or knowledge about the inner workings of a DAO are so hard to come by that only a small group of actors can implement smart contract changes, but otherwise the ownership of governance rights is widely distributed, and processes are automated to a large extent, then the DAO is at the fourth stage of our spectrum (4). The important thing here is that governance and spending decisions do not rely on a group of people, but are automated.

We’re now entering centralized territory. DAOs on that end of the spectrum are well advised to seek out competent counsel and are most likely best off by incorporating at least parts of their operations as SubDAOs with legal wrappers, depending on their individual circumstances.

A little further towards centralization (5) we have a DAO with some sort of leadership. The actual person in charge varies and most DAO activities are run by smart contracts that are updated or amended from time to time by a wide variety of actors. The important thing here is that not the same group is in charge of protocol development for too long, otherwise it could be argued that the DAO is at the mercy of one development team, and is actually their product. At this stage control of the DAO is fluid, but there still is someone in control of aspects or the whole of the organization.

In its fully decentralized state (6), no one has control over the whole DAO, it moves according to immutable conditions baked into its smart contracts. But of course, every party that interacts with specific functions, or services the DAO offers, has control over what goes into these services and control over which functions are performed for him.

We can see that control becomes more and more centralized and existent as we go from right to left in our spectrum of decentralization. Apart from control we have discussed six main areas to consider and wanted to offer DAO governance a sort of matrix where they can fine-tune their decentralization gauges and create action items of how to become more decentralized if they want to do so. The matrix was inspired by a product of Balloonist.xyz as a contribution to the DAO/DeFI ecosystem.

5. Decentralization in the US

How does US regulation currently define decentralization?

The US currently has no regulation in place that provides a formal definition of decentralization or the legal implications of satisfying that definition. Various legal papers and proposals, however, have sought to define decentralization and have largely concluded that sufficiently decentralized networks should be exempted from security registration as defined by the Securities Act of 1933.

The SEC has argued that DAO tokens qualify as securities when token holders do not have effective voting rights or rely on the managerial or entrepreneurial efforts of an “active participant.” According to Georgetown Law’s Legal Wrappers and DAOs, DAOs may seek to avoid classification by implementing a fully decentralized governance structure akin to a general partnership. However, general partnerships can introduce potential unlimited liability, which shows the limits to the current regulatory regime.

In an effort to provide clarity, Rep. Patrick McHenry introduced a bill, Clarity for Digital Tokens Act of 2021, that would create an exemption from registration under a new Section 4B to the Securities Act of 1933 (to be called “Token Safe Harbor”) for the offer and sale of a token if: (i) the initial development team intends for the network on which the token functions to reach network maturity within three years after the first token sale, (ii) the token is offered and sold for the purpose of facilitating access to, participation on or the development of the network and (iii) the initial development team complies with certain disclosure and filing requirements.

The bill defines network maturity as the status of a decentralized or functional network that is achieved when the network meets the standard of either control or functionality. Under the control standard, the network must not be economically or operationally controlled. Specifically, networks of which the initial development team owns more than 20 percent of tokens or owns more than 20 percent of the means of determining network consensus do not meet the requirements. Under the functional standard, network tokens must be used for transmission and storage of value on the network, the participation in an application running on the network, or otherwise in a manner consistent with the utility of the network.

Ultimately, the determination of network maturity is left up to legal analysis at the end of the three-year period, for which dimension thresholds are not fully defined. This legal analysis must include (i) a description of the extent to which decentralization has been reached across a number of dimensions, including voting power, development efforts, and network participation and (ii) an explanation of how the initial development team’s pre-network maturity activities are distinguishable from the team’s ongoing involvement with the network.

Other legal papers seek to provide more clarification. A Legal Framework for Decentralized Autonomous Organizations, published by Andreessen Horowitz, provides this definition for decentralization: “Decentralization of a given protocol occurs when control (e.g., governance) of the non-immutable aspects of a protocol’s smart contracts is passed from the developers to the members of a DAO via the activation of governance smart contracts.” Crypto protocols often implement decentralization progressively, however, by staggering the release of tokens or maintaining control of certain aspects of the protocol to mitigate security risks. Protocols that progressively decentralize enter into a legal gray area during which they may qualify as a U.S. incorporated entity that is directly responsible for the valuation (and appreciation) of its governance tokens. The implications of this qualification include a responsibility to file tax returns and register tokens as securities. The proposed “Token Safe Harbor” section specifically addresses this ambiguity.

While the Clarity for Digital Tokens Act of 2021 clearly outlines the exemptions available to networks that qualify as decentralized, additional US regulatory clarity is required on the specific dimension thresholds that a network must reach in order to qualify for these exemptions.

6. Decentralization in the EU

The European Union currently has no framework in place specific to matters related to crypto-asset issuers and service providers. This will change when the proposed MiCA (Markets in Crypto-Assets) enters into force in 2024.

With this regulation, the European Commission attempts to create a tailor-made regulatory framework for all crypto-asset issuers and service providers. In its first proposal, MiCA does not mention decentralization and does not put any framework into place for the regulation of DAOs. For instance, the offering of crypto-assets or the provision of crypto-asset services requires the issuing or providing entity to be a legal person, a feat which cannot be achieved by a truly decentralized organization.

However, some drafts published during the process of creating MiCA show that the European legislator is not oblivious to the existence of DAOs. In a draft published by the European Parliament, multiple mentions of DAOs have been made. For example, a definition of DAOs had been added to the proposal, defining Decentralized Autonomous Organizations as “a rule-based organizational system that is not controlled by any central authority and whose rules are entirely routed in its algorithm”. With this definition, the European Parliament holds quite a broad perspective to what constitutes a DAO. Organizations qualifying as a DAO can on the basis of the proposal by the European Parliament, without being a legal entity, also issue crypto assets.

In a new report published by the European Commission, the ‘European Financial Stability and Integration Review 2022’, a chapter was dedicated to DeFi protocols. In this report, the Commission has called for a reconsideration of the current regulatory approach. A potential new regulatory approach would implement more activity-based regulations instead of entity-based regulations. The European Commission wants to focus the regulation on the smart contracts, and to target the developers that have created those contracts, holding them accountable for their creation.

7. Offshore incorporation

The dYdX foundation recently published a blog post and an adjacent paper about how they incorporated their grants DAO as a purpose trust in Guernsey, one of the British Channel Islands.

Guernsey offers competitive tax rates and trusts there have minimal reporting requirements. The idea is to make ongoing operation as painless and to give token holders as much governing rights as possible.

An important limitation of the Guernsey trust model is that dYdX only developed it for subDAOs focused on a specific task, and not as a wrapper for the whole operation. dYdX is of the opinion that a similar structure could wrap all of the DAO, although the a16z paper contradicts that opinion.

One important caveat here is if the DAO maintains significant relations to US members or customers. US agencies have displayed their willingness to engage with DAOs based on only minimal US involvement, so this caveat might be a bigger deal than it seems, especially if taxes are likely to be due in the United States.

The Guernsey trust is only indicated if:

- The protocol is governed by token holders.

- The purpose trust is a vehicle for a subDAO focused on a particular task, such as making grants, and does not wrap the DAO.

- There should be a legally compliant structure that does not require ongoing filings.

- Taxes should be as low as possible

David Kerr, the lead author of a16z’s paper, points out that US members might face considerably more difficulty in filing taxes from proceeds of a DAO that is incorporated in Guernsey, the British Virgin Islands or other tax havens, because tax treaties between the US and these legislations are absent or significantly reduced. Taxes due could also be much higher than the federal tax rate of 21%.

Kerr opines that DAOs would do well to incorporate in the US. We suggest that this needs input from qualified counsel and careful research in which jurisdictions and regulations a DAOs activity fall under. It is highly unlikely that incorporation in the US would exempt a DAO from incorporation or regulatory compliance in all other jurisdictions where it has a considerable number of customers or contributors.

We will not get into further detail about this topic, because it clearly merits its own article and dilutes the focus of this blog post. If DAOs feel the need to incorporate they should employ legal counsel straight away. The sheer lack of clear regulatory guidance might mean that even best efforts are only short-term solutions.

These DAOs could also be seen as Passive Foreign Investment Companies (PFIC). Investopedia reminds us that “investments designated as PFICs are subject to strict and extremely complicated tax guidelines by the Internal Revenue Service, delineated in Sections 1291 through 1298 of the U.S. income tax code.”

Offshore incorporated DAOs might face difficulties in attracting investments from the United States as a result. The overall implications of offshore vehicles for DAOs is beyond the scope of this blog post and we advise DAO governance to engage with qualified counsel before going that route.

8. Conclusion and Outlook

“Que Sera, Sera”, as Doris Day sung in her wonderful rendition that first appeared in Alfred Hitchcock’s “The Man Who Knew Too Much”.

We definitely do not know much about how regulators will interpret decentralization in the future, or try to apply existing legislation, and how this will affect DAOs, their stakeholders, and decentralized organizations in general. So, we have to take Doris Day’s advice and say: “What will be, will be!”

Our research here is meant to illustrate the current situation and the kind of thinking regulators have expressed to date. We can assume with some certainty that MiCA will inform other regulations and that completely decentralized operations will remain outside the scope of individual jurisdictions. We hope that visualizing what the spectrum of decentralization looks like can help DAO governance to position their organizations where it makes the most sense to the organization, but also to society as a whole.

Please feel free to reach out to the authors with any questions you may have. We view this research as a basis for ongoing discussion and further inquiry into this fascinating topic.

9. About the authors

Watsonlaw is a young, progressive firm with extensive experience in the field of crypto regulation. With modern, innovative out-of-the-box solutions for all regulatory obstacles crypto-oriented companies have to overcome, we help all our clients create possibilities and reach the optimal outcome for their businesses. In addition to knowledge of all applicable regulations, we also possess broad experience in supporting all clients, whether they are small, medium or large size companies, in setting up their business, drawing up all necessary contract documentation and going through licensing and/or registration procedures with the relevant regulator.

If you have questions regarding your crypto-oriented company, do not hesitate to contact us at w.smits@watsonlaw.nl or at +31 088 440 2200. Watsonlaw is your partner in blockchain, tokenization and the crypto market in the Netherlands and abroad, with a broad network of collaborating law firms throughout various countries to provide national as well as international advice. The lawyers of Watsonlaw can guide your company every step of the way to becoming a leading blockchain enterprise.

Flipside Governance is the DAO governance arm of Flipside Crypto a blockchain data and business insights company from the United States with a global, distributed workforce.

Flipside Governance is active in more than a dozen DAOs and is a recognized delegate of MakerDAO, Aave, Optimism and Hop Protocol.

Helping DAOs design governance from the ground up and being actively involved in the day-to-day operations as well as publishing research around central topics of governance, is Flipside Governance’s daily bread.

You can find our research here on Medium and reach out to us on Discord or Twitter.